If the IRS has already levied your bank account, many taxpayers immediately ask the same question: will the IRS take more money?

The answer depends on the amount owed, the status of the collection case, and whether the underlying tax issue is resolved.

I work directly with taxpayers facing IRS collection enforcement, including bank levies, wage garnishments, tax liens, and other serious collection matters.

Schedule a consultation regarding your IRS collection situation.

What Happens After an IRS Bank Levy?

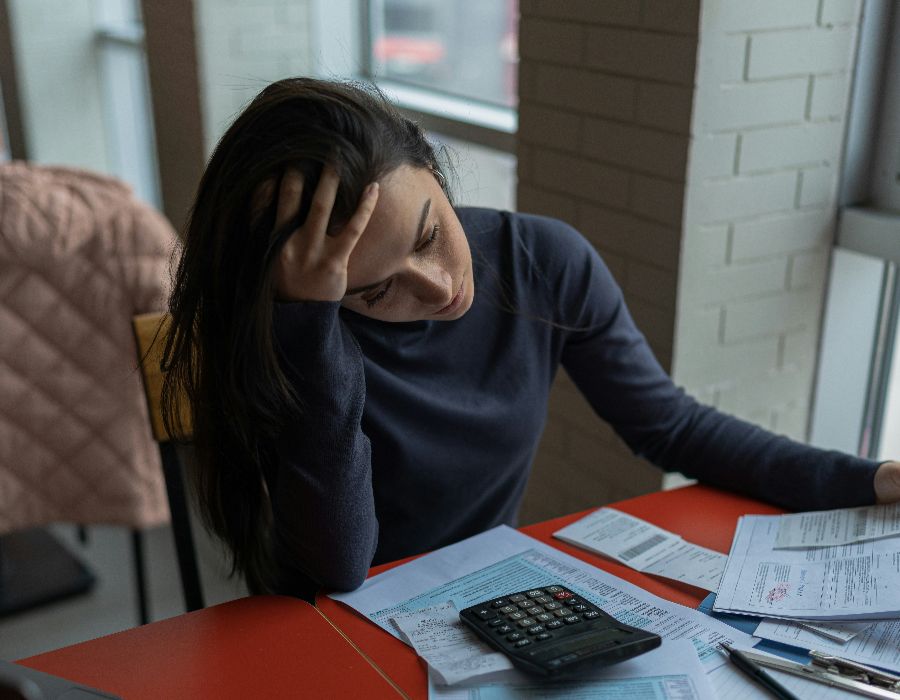

An IRS bank levy is often one of the most stressful collection actions a taxpayer can experience. Funds become frozen, automatic payments may fail, and access to money can suddenly disappear.

However, many taxpayers are surprised to learn that the levy itself is often not the end of the collection process.

One of the most common questions is whether the IRS will take more money after a bank levy.

In many situations, the answer is yes. If the tax debt remains unresolved, additional collection action may occur.

Understanding what happens after an IRS bank levy can help taxpayers avoid further financial disruption and take steps toward resolving the underlying problem.

What an IRS Bank Levy Actually Does

An IRS bank levy generally freezes the funds that are in the account when the bank receives the levy notice.

The bank typically holds those funds for approximately 21 days before sending them to the IRS.

During that hold period, taxpayers may still have limited opportunities to address the situation depending on the facts of the case.

Once the funds are transferred, the IRS applies them toward the outstanding tax debt.

Many taxpayers mistakenly assume that once this happens, the IRS collection matter is finished.

Unfortunately, that is not always the case.

Will the IRS Take More Money After a Bank Levy?

Possibly.

If the levy does not fully satisfy the balance due, the IRS may continue collection efforts.

For example:

- The taxpayer owes $50,000

- The levy collects $3,500

- A balance remains outstanding

The IRS may continue pursuing collection of the remaining debt.

Future enforcement can sometimes include:

- Additional bank levies

- Wage garnishment

- Federal tax liens

- Revenue officer involvement

- Business collection enforcement

The important point is that the IRS generally focuses on collecting the entire balance, not simply the amount obtained through one levy.

Can the IRS Levy the Same Account Again?

Yes.

Many taxpayers are surprised to learn that a bank levy is not necessarily a one-time event.

If a balance remains due and the collection issue is not resolved, the IRS may issue another levy later.

The IRS may also identify other accounts or collection sources.

For a more detailed discussion, review How Many Times Can the IRS Levy Your Bank Account?.

Repeated levies can create significant financial hardship, especially when taxpayers continue to ignore IRS notices after the first levy occurs.

What Happens During the 21-Day Holding Period?

After the bank receives the levy notice, frozen funds are generally held for approximately 21 days.

During that time:

- The money remains frozen

- The bank restricts access to the funds

- The IRS has not yet received the money

- The collection case remains active

This period is often one of the last opportunities to evaluate possible solutions before the funds are transferred.

Waiting until after the holding period expires may reduce available options.

Why Additional Collection Activity Often Follows

A bank levy rarely occurs in isolation.

In most situations, the IRS has already:

- Assessed the tax debt

- Sent multiple notices

- Issued collection warnings

- Provided opportunities to respond

By the time a levy occurs, the case has usually reached an advanced stage of the collection process.

If the underlying problem remains unresolved, the IRS may continue moving forward with enforcement.

This is why taxpayers should view the levy as a symptom of a larger collection issue rather than a stand-alone event.

Common Mistakes Taxpayers Make After a Levy

After a bank levy occurs, taxpayers sometimes make decisions that increase the likelihood of future enforcement.

Common mistakes include:

- Ignoring the levy after funds are taken

- Assuming the matter is over

- Failing to address missing tax returns

- Avoiding future IRS correspondence

- Waiting months before seeking assistance

Unfortunately, these delays often allow collection problems to grow.

Interest and penalties may continue to accrue while enforcement risks remain active.

Warning Signs More IRS Collection May Be Coming

Some indicators that additional enforcement could occur include:

- A remaining tax balance after the levy

- Unfiled tax returns

- Recent Final Notices of Intent to Levy

- IRS revenue officer contact

- Prior defaulted payment plans

- Multiple years of unpaid taxes

When these factors are present, taxpayers should recognize that the collection case may still be escalating.

How Taxpayers May Address Future Collection Risk

The most effective way to reduce the risk of additional levies is usually to address the underlying tax issue.

Depending on the facts, possible options may include:

- Installment agreements

- Offer in Compromise evaluation

- Currently Not Collectible status

- Penalty abatement requests

- Filing missing returns

- Collection appeals

Every IRS collection case is different, and available options depend on the taxpayer’s financial circumstances, compliance history, and overall collection status.

For additional information about available solutions, visit IRS Tax Relief.

Understanding the Bigger Collection Picture

Many taxpayers focus exclusively on the frozen account.

While that reaction is understandable, the larger concern is often the unresolved IRS debt itself.

Without addressing the underlying issue, the IRS may continue collection activity long after the first levy occurs.

Taxpayers should therefore evaluate the entire collection situation rather than focusing solely on the money that was frozen.

For levy-specific information and potential options, visit IRS Bank Levy Help.

Do Not Assume the First Levy Is the Last

One of the biggest misconceptions about IRS collection enforcement is that a single levy ends the matter.

In reality, additional collection activity may occur if a balance remains outstanding.

The first levy often signals that the IRS has already moved into active enforcement mode.

Understanding what happens after an IRS bank levy can help taxpayers recognize the importance of addressing the broader tax issue before collection pressure increases further.

Take Action Before Additional IRS Collection Occurs

If the IRS has already levied your bank account, waiting may increase the risk of future collection activity.

Additional levies, wage garnishments, tax liens, and other enforcement actions may become more likely when the underlying tax problem remains unresolved.

GMD Tax Law helps taxpayers evaluate IRS collection matters, levy situations, and potential resolution options.

Schedule a consultation regarding your IRS collection situation.